This thought leadership piece – and the related blogs that will explore key topics – will outline why, in the post-COVID-19 era, marketplaces will prove a crucial operating area for banks. We will illustrate how some leaders have ventured profitably into this space, and will explain the steps banks can take to create marketplaces of their own.

Summary

- The Fourth Industrial Revolution, which is defined by the platform economy, is underway. This is a profound shift, and banks need to respond.

- At the same time, consumers increasingly expect hyper-relevance from every interaction – which platforms can bring.

- In a world where traditional revenues are shrinking, banks must adopt platforms to deliver services and products.

- Ecosystems and marketplaces provide the ideal space for banks to meet customers’ needs by onboarding partners and facilitating the end-to-end delivery of offerings.

- A marketplace approach benefits banks, consumers and partners – with Alibaba and Amazon proven leaders in this space.

- Marketplaces are digitally driven, one-stop-shop platforms that focus on product or service comparisons, and that banks can use to fulfil their customers’ life needs seamlessly. Banks can either set up their own marketplace or offer their products through other marketplaces.

- Although marketplaces might fall outside their comfort zone, banks have significant advantages: customers trust banks; they are already at the centre of their customers’ lives, and they have a range of suitable payments products available.

- The following steps are crucial for banks looking to undertake their marketplace journey:

- Define a marketplace strategy;

- Design from the customer to the customer;

- Decide on the e-commerce platform and capabilities that best fit requirements.

- Partnering with other players and building coalitions are at the heart of successful marketplaces.

- In a post-COVID-19 world, the leaders will be those banks that pursue revenue growth strategies, play a volume strategy game and compete to be hyper-relevant. This battle will play out in the platform economy.

1) A Changed World

“Banking is necessary; banks are not.” This quote, attributed to Bill Gates, has been common currency for three decades and earned a new lease of life with the rise of fintechs and the GAFAA firms. Its crux is that the world can’t operate without banking, but it can get by without the players that traditionally offer such services.

That much is true. Banks face an existential threat as others move on to turf that for generations has been exclusively theirs. Yet while banks are aware of this, it’s also the case that most still do what they’ve always done: provide banking products and services. Granted, many such offerings are available via digital channels, but simply digitising existing banking products and services isn’t enough.

To survive and thrive, banks must think about their role and how they can expand their functions to stay relevant in their customers’ lives. As Accenture has written elsewhere: “The big banks that succeed … will be those willing to transform themselves by shedding the old versions of themselves in favour of something quite different.”[1]

What does “different” require? It requires that banks extend their reach and create ecosystems that offer hyper-relevance and a market of one for each customer. In short, it requires becoming a Living Bank.[2] In this way, they can provide “a deeply personalized ‘me-centred’ experience wherever, whenever and however the customer wants.”[3]

Before looking at the practicalities involved in reaching that state, it’s worth highlighting banks’ powerful inherent advantages. First, their customers trust them. Second, they have brand-recognition and can attract worthy partners. And third, banks are already part of their customers’ lifestyles and know them well – they have the data on what their customers earn, where they spend their money, and much more besides; that’s not the case for firms that sell, for instance, consumer goods.

In other words, banks are supremely well-positioned to take advantage of digitisation and the advanced technologies that are underpinning the shift in the global economy from the Third Industrial Revolution (driven by computing and communications technology) to the Fourth, defined by the platform economy.

Some already have. As customers increasingly expect hyper-relevance from every interaction, platforms like AutoFi – a US-based fintech whose e-commerce platform lets customers look for, buy and finance a car (through banking partners) wholly online – offer a way for banks to meet that need. It is the sort of customer-centric, ecosystem-driven space that creates hyper-relevance for customers, and perfectly represents where banks need to be.

The future of banking: Time to rethink business models. An Accenture report outlines new banking business models that enable banks to reconfigure themselves to keep pace with disruption.

LEARN MOREBeyond banking

Banking, then, is changing fast, and leading banks are shifting from providing core banking-centric services to delivering customer-centric services. The following three factors underpin this:

- The demand for service aggregators. Customers are reluctant to go to one place to view a product, another to secure finance and a third to get insurance – even for large purchases like cars and, in some cases, homes. Platforms like AutoFi solve that.

- The approach of GAFAA firms and neobanks, which focus on the experience factor to win customers’ hearts. These high-tech competitors are moving into this space, while capitalising on, and even cannibalising, banks’ offerings and services in ways that aren’t visible to customers.

- The acceleration of change due to the internet and e-commerce. Over the past decade, numerous financial start-ups have launched marketplaces, while GAFAA firms offer a range of banking services.

On top of that, the “new normal” is here – COVID-19 has forced banks to digitise faster than expected, with the ability to adapt to this change differentiating leaders from laggards. The pandemic has ushered in the “Never Normal” era in which the social and structural norms that the world built up in the 20th century – being able to go to school, to work, to the shops, to entertainment venues – have been overturned. COVID-19 has changed the status quo. Our view is that people will continue to accept new norms at an increasingly rapid pace, as long as the benefits of doing so are clearly articulated.

From a societal standpoint, then, the future will see more adaptive and accepting consumers even as the platform economy continues its ascent. And with banking one of the industries most susceptible to future disruption, banks must accelerate their response and think beyond offering standard financial products and services.

Why Banks?

The Fourth Industrial Revolution is affecting nearly every industry – so why are the opportunities particularly good for banks?

It’s because succeeding as a Living Bank requires, in part, creating a “market of one” for every customer, and banks are among the few that already tick that box: each customer has a unique profile and position. And even though banks group their customers, the data for each – from accounts to portfolios to transactions – is unique.

This means banks not only have the data necessary to create markets of one; they also have the ability and the funding to create such platforms.

Yet success requires more than offering a platform. What counts is the value generated from the services offered, with the greatest value achieved by adjusting every requirement that each customer might have: providing what they want and ensuring they can pay in the manner most useful to the them. Short of logistics, there is no reason why banks can’t provide the bulk of the end-to-end delivery of products and services – whatever those might be.

That means becoming their customers’ financial planners – helping them, for instance, to plan their dream vacation, buy their next car or browse for new home appliances. That’s best achieved via marketplace ecosystems: online spaces where banks onboard partners and facilitate the end-to-end (E2E) delivery of offerings.

The benefits of this approach are numerous:

- Banks win financially and from increased loyalty because, by positioning themselves at the centre of their customers’ lives, they can bring products closer to them to enable a new relationship and ensure they become a one-stop-shop for their customers’ needs.

- Customers benefit by accessing credit and flexible payment instruments conveniently, and from personalised experiences.

- Partners gain from access to an audience of customers ready to purchase, and from lower marketing spend per acquisition.

2) The Rise of the Marketplace

The global leaders in the marketplace platform space are Amazon and Alibaba. Along with their multitude of offerings, both marketplaces provide financial services: Amazon uses marketplace data to assess risk for loans, while Alibaba brings together a range of banking ecosystem propositions under its umbrella. Data analysis and cutting-edge technology are at the heart of both firms’ approaches.

As these examples show, marketplaces are digitally driven, one-stop-shop platforms that focus on product or service comparisons and provide a range of offerings. Banks can use them to help their customers seamlessly fulfil their life needs.

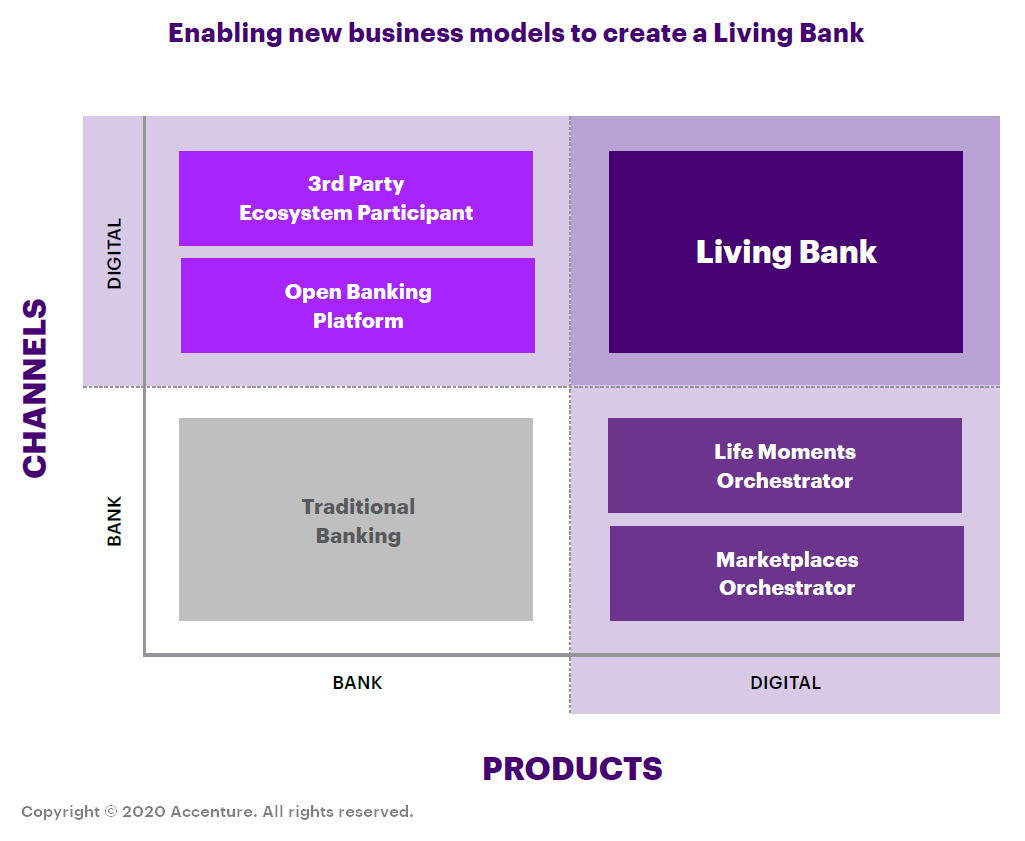

As banks move away from the shrinking opportunities provided by traditional banking and undertake the journey to become Living Banks, there are a number of solutions they can employ (see chart).

Evolving to become a Living Bank – the point at which banks are consistently relevant to their customers, and where they embed vitality by delivering that “hyper-relevant, ‘me-centred’ customer experience across a range of physical and digital channels”[4] – is a journey that culminates in banks providing E2E financial services to their customers from a single platform under a subscription model.

That state looks a long way off for most, yet the following product and channel solutions can help them move closer to it:

- Life moments orchestrator: The bank orchestrates its own ecosystem built around specific life moments, like buying a house or car.

- Marketplace orchestrator: Where the bank sells – either by white-labelling or co-branding – non-financial products to its customers.

- Third-party ecosystem participant: This channel solution sees the bank offer its own financial products to a third-party’s customers via that third-party’s platform.

- Open banking platform: Banks can leverage open application programming interfaces (APIs) to enable partners to incorporate products, data and/or specific processes in their value propositions.

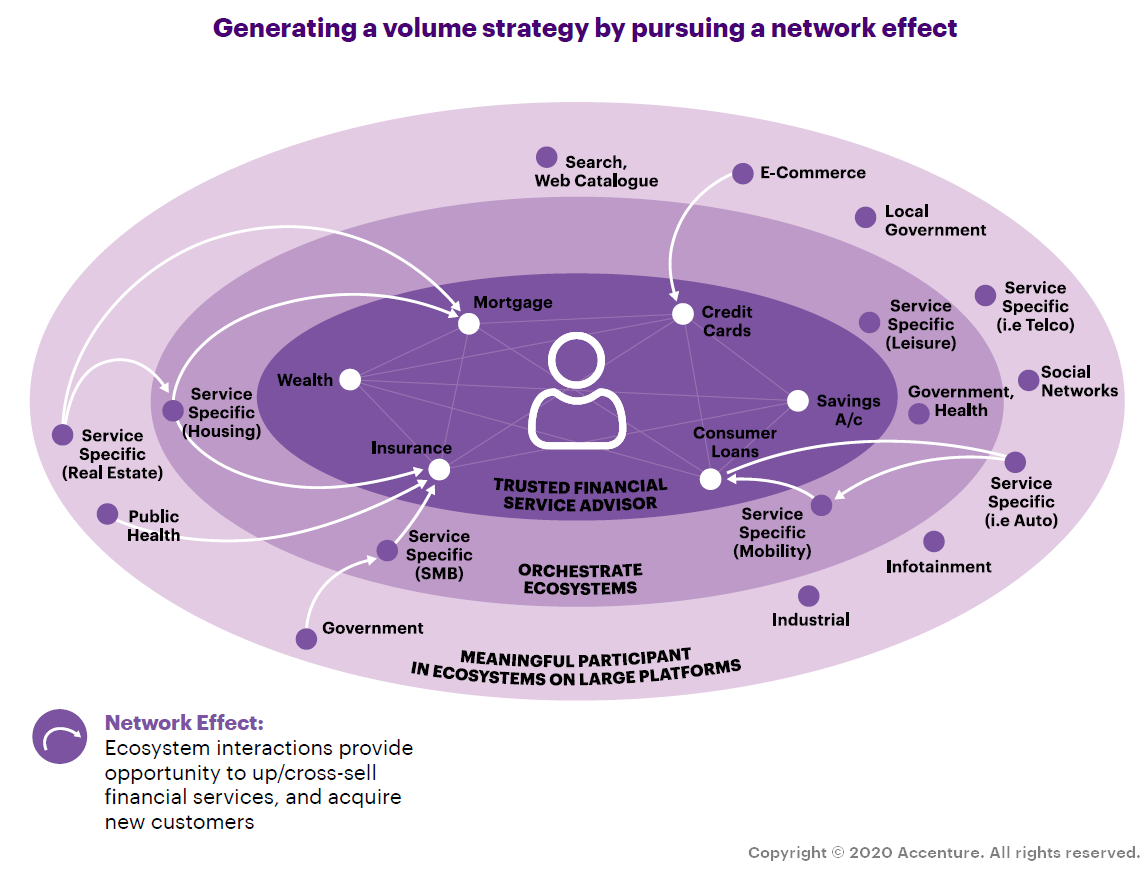

These business models help banks generate a volume strategy and create a network effect in which different ecosystems interact (see diagram), providing the opportunity to up-sell and cross-sell financial services, and to acquire new customers.

Although the marketplace approach lies outside many banks’ comfort zones, they are well-placed to make this happen: they can offer their products through the marketplaces of others, and they can set up marketplaces of their own to bring their products closer to customers. In this way, they can create an ecosystem of partners.

As we’ve seen, banks come to this with some significant advantages. First, their customers trust them. Second, they are already at the centre of their customers’ lives. And third, they have flexible payments products that they can offer across those customers’ journeys.

Some have acted already. China’s ICBC, for example, has its Mall offering – an online B2C and B2B marketplace that offers a vast range of goods. Its B2C Mall in Argentina, for instance, includes household appliances, consumer electrical items, fashion and beauty products, as well as educational courses, holidays and car accessories.[5] Spain’s BBVA is another venturing into new realms: as part of its digital transformation, it is exploring the idea of offering banking products on Amazon, adding that it “recognises that financial institutions must adapt to this way of selling”.[6]

Singapore’s DBS is also among the leaders in this space. Its marketplace allows consumers to buy or rent property, book flights or hotels, switch their electricity supplier, or buy or sell a car.[7] Its car marketplace provides a one-stop-shop where consumers can browse available vehicles from dealers or owners, and save money on a car loan, vehicle insurance and fuel.[8]

Unleashing the Power of Data

Data plays a crucial role in marketplaces by helping banks to understand their customers better, and ensuring they know in real-time what customers are doing and their life experiences.

This brings hyper-relevance for both parties, ensuring that the bank can increase conversions and the customer can finalise tasks.

Banks can boost this further by integrating their marketplaces with social platforms to create a data-driven marketplace with rigorous campaign management and optimal up-sell and cross-sell capabilities.

Additionally, given the uncertainty and inherent asymmetry of information for buyers and sellers in marketplaces, a data-driven trust network is crucial to resolve key challenges. Buyers, for instance, want more information about the authenticity of what they’re purchasing, while sellers need to know whether buyers are creditworthy.

We will dig deeper on data-driven trust networks in one of the blogs that will accompany this paper. For now, it’s sufficient to say that banks can leverage data to provide such networks, offer better and more-personalised services, and further help meet the needs of existing and future customers – and can profit from doing so.

As these examples show, marketplaces allow banks to move up the digital chain as they seek to become a Living Bank, providing a way for them to extend their involvement in their customers’ lives and, by doing so, create new revenue pools and become more resilient.

3) How to Build a Marketplace

Many banks want to follow the marketplace path, but don’t know where to start. The following three areas are crucial:

- Define a marketplace strategy at the intersection of customer-centricity and business goals;

- Design from the customer to the customer – with simplicity for the customer at the core;

- Decide on the e-commerce platform and capabilities that will prove the best fit for its marketplace vision and banking architecture, with data at the core of this.

1. Define a marketplace strategy

The first stage in creating a marketplace is to define the platform business model that the bank wants – B2B (like Alibaba), B2C (Amazon) or P2P/C2C (eBay). The first model is a relationship-driven option whose customers are businesses; the others are product-driven platforms targeting individuals and households. Whichever model the bank chooses, it must be carefully designed to complement the bank’s offerings, and it must encapsulate services around each proposition.

Next, it must reconsider how its business model should change to evolve from a traditional bank that provides straightforward banking instruments (accounts, credit cards and loans) to a financial partner offering products (cars, houses, jewellery) and services (travel, weddings, education) that are wrapped with banking instruments.

The next step is to consider three related areas:

- Marketplace type: Will it be vertical, focusing on a specific area or niche – like a sports brand – offering a depth of products from a few expert sellers? Will it be a horizontal marketplace, whose offerings are wide-ranging and generalist yet share characteristics, like the supermarket Carrefour? Or will it be a global marketplace, like Amazon or Alibaba, that sells everything, connecting buyers and sellers from across the world?

- Target audience: Will it focus on its retail customer base? On any retail customer? On SMEs or corporates?

- Products and services: Will the marketplace offer new retail products or repossessed products? Or will it promote business and payments solutions?

The next stage is for the bank to define its ecosystem, consider how its partners will operate their platforms, and determine how its ecosystem can contribute to other platforms. For example, the bank’s ecosystem could offer credit cards, loans and other financial products for individuals and businesses, and engage with partners’ platforms by offering payments infrastructure as well as KYC and risk-scoring algorithms. At the same time, those partners can drive data and other products and services to the bank’s ecosystem, benefiting all parties.

The final step is to define the bank’s position on areas like fulfilment, after-sales service and customer support, and then determine which business, operations and customer care processes it must add or adjust.

2. Design from the customer, to the customer

Living Banks succeed by designing with the customer experience front and centre. Consequently, marketplaces must be designed as a venue that is not business-focused but customer-focused, providing a space for the bank to bring products to customers.

Doing so means that as soon as the customer enters the marketplace – and even before, in the case of partnerships and integrating with social media platforms – he or she represents the key focus for the bank, which can offer every necessary service without that customer having to go anywhere else.

3. Decide on the e-commerce platform and capabilities

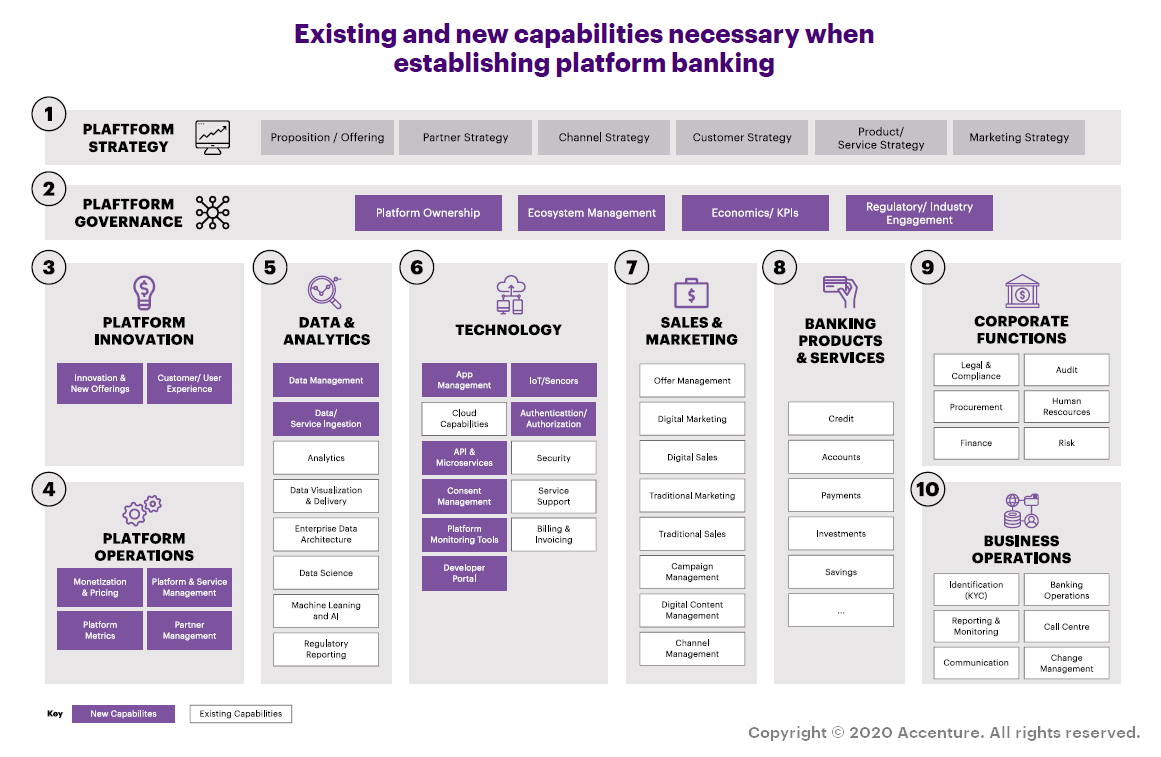

Pursuing a marketplace solution requires that banks create specific new set-up capabilities to deliver and sustain platform banking. That starts by assessing their existing capabilities with a particular focus on platform-related areas like governance, innovation, and data and analytics. As the chart below shows, the areas in which banks will find they fall short are largely technology-related.

Next, banks must activate a number of enablers to pursue their platform agenda. Among these: design first and foremost for a mobile customer experience; use analytics and AI-powered connected experiences to optimise hyper-relevancy; use bots to provide meaningful, fuss-free interactions for customers; create an API factory; and measure progress using a new KPI structure.

These enablers allow the bank to form individualised value propositions that link to key life moments and customer interests – all based on data. For example, should the platform determine that a customer is about to buy a house, get married or have a baby, it can provide a catalogue of relevant products and services, complete with coupons and discounts.

These individual moments integrate further with customer journeys to ensure the bank can communicate in the best way possible for a range of events – from vital situations (like getting married, inheriting money or starting a job) to day-to-day experiences (financial planning or taking out insurance), and from moments of truth that create the opportunity to generate satisfaction (the loss of a credit card) to business-as-usual events like paying bills. Doing so has a range of positive consequences, including building customer loyalty, as we shall see in one of our blogs in the series.

Finally, it’s worth noting that coalitions are foundational to successful marketplaces, which are attractive to potential partners. We’ve noted earlier the clear benefits for banks, but other participants gain too. Take insurance companies: the value proposition includes being able to cross-sell products and capture leads at specific customer life moments. We will look in more detail at this aspect in a subsequent blog.

Smooth Sailing? Not Always

Dealing with complications is part and parcel of the marketplace process, which is why banks must consider a range of factors in areas like operational, legal and compliance – including viewing these aspects through the risk lens. The broad question they must answer is how to operate in this space while protecting their brand.

In 2020, for example, Santander Consumer USA – the US’s biggest subprime car lender, which is majority-owned by Spain’s Banco Santander – agreed to pay a settlement of US$550m after state authorities said it had used deceptive lending practices.[9]

The settlement came after the firm was accused of knowingly exposing borrowers “to unnecessary risk and placed them into loans with a high probability of default”.[10] In response, the bank said it had strengthened its “risk management across the board – improving our policies and procedures to identify and prevent dealer misconduct, and tightening standards to ensure affordability”.[11]

In any marketplace, then, partnering is a crucial element for banks to consider. Less obvious factors include aspects like logistics. Banks aren’t in the logistics game, and the purpose for banks of a platform that sells white goods, for instance, is to connect merchants with consumers. However, consumers buying from such platforms aren’t likely to distinguish between the bank and the vendor in the event their purchase goes missing or is delayed, and that can carry reputational risk and administrative hassles.

In short, a successful platform marketplace means determining how to operate in this space while protecting the brand. That holds as true for banks – and perhaps more so for banks – as it does for any player. At the heart of this approach, lies the strategic question: What kind of a business will I become?

4) Taking Action

The changes sweeping through the banking sector leave players with one of two choices: take action, as some have done, or do nothing and hope that will suffice. The problem with the second course is that it won’t. Banking faces significant disruption, and it is highly susceptible to it – and that means players are in a fight for survival.

The coming years will see the emergence of leaders that pursue revenue growth strategies, play a volume strategy game and compete for hyper-relevance in their customers’ eyes. This battle for dominance will be played out in the platform economy, with innovation boards crucial to generate the required mobilisation and focus. Banks that embrace the philosophy of “simplicity for the customer” as their North Star are the most likely to succeed.

This paper will be accompanied by blogs that look deeper at some of the issues raised. The first of these will assess how to build the customer value proposition and outline key considerations for banks looking to create a successful marketplace. It will also explain what loyalty means in the context of the marketplace, and explain how marketplaces promote that key attribute.

Want to know more about how Insurers can make a wise pivot using Banking Marketplace? Read our comprehensive paper titled, “Banking Marketplace: Making a wise pivot”.

Subscribe for more from Accenture Banking.