More than five years after the launch of Apple Pay and four-plus years after the US POS liability shift for EMV, the US market finally appears set to fully embrace contactless payments. To date, consumer adoption of contactless payments (also known as tap-to-pay, or dual-interface EMV) has been inhibited by low penetration of contactless technology among both issuers and merchants. But based on recent market observations and the latest data from Visa, the landscape appears to be shifting.

In the last 18 months, the three largest US debit issuers (Wells Fargo, Bank of America and Chase) and the six largest US credit issuers (those above, as well as Citibank, Capital One and U.S. Bank) have increased their issuance of dual-interface EMV cards across their portfolios. Visa now expects 300 million of these contactless-capable cards to be in circulation in the US by the end of this year and several of the largest banks are already running promotional incentive campaigns to spur usage. This is in addition to these banks’ existing participation in tap-to-pay digital wallets such as Apple Pay.

Merchant acceptance of tap-to-pay transactions is also increasing, with Visa reporting that 69 percent of face-to-face transactions now occur at contactless-enabled merchants, up from 60 percent last year. Most EMV terminals shipped since 2015 have contactless functionality, and after some initial hesitation, more merchants in high-volume categories (drug, grocery, quick-service restaurants) are now turning on the capabilities.

Learn how Accenture supports Women in Payments, a growing network that unites women in payments from around the globe.

LEARN MOREWhen similar dynamics appeared in international markets, the growth of contactless payments inevitably followed:

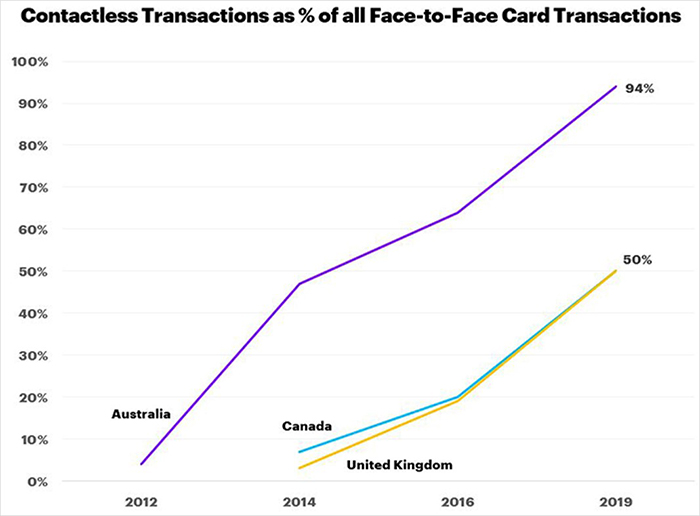

- Contactless transactions in the UK have grown at an average rate of more than 80 percent since dual-interface issuance accelerated in 2013. Contactless transactions now represent about 50 percent of all face-to-face card transactions, despite being limited to small-value purchases (less than £30).

- Canadian contactless volume grew at an average rate of 65 percent from 125 million transactions in 2011 to 4.1 billion in 2018. Contactless now represents the majority of all face-to-face card transactions.

- Australia is perhaps the most stunning example, with contactless transactions representing 94 percent of all face-to-face card transactions. This is due to an early contactless mandate from Mastercard, which spurred widespread adoption and market penetration in parallel with EMV adoption in 2011–2012.

Contactless growth is not just the result of a share shift from contact to contactless. It is also a catalyst for the ongoing shift from cash to electronic payments, especially for small-ticket transactions—Visa data shows an approximate 20 percent lift in transactions per card in “mature” contactless markets. Although any such benefits will take several years to fully develop, incremental transaction growth of even a few percentage points for a regional retail bank issuer (e.g. $5 billion annual credit spend, $20 billion annual debit spend) could generate up to $10 million in additional interchange revenue each year.

Now that the market dynamics for contactless growth are finally in place and the largest issuers are moving aggressively, other industry stakeholders must consider several important strategic questions:

- What is the ROI and business case for super-regional and regional issuers to issue dual-interface cards, what factors could improve those assessments and how do contactless payments fit into a broader portfolio payments growth strategy?

- What is the impact to issuers of mobile digital wallets (e.g. Apply Pay, Google Pay), which accelerate contactless payments adoption but can obscure issuer branding and take a share of the per-transaction economics?

- What is the impact to merchants’ cost of payments acceptance, including their ability to route debit transactions to the network of their choice at contactless-enabled terminals?

- In conjunction with contactless payments, what other potential form factors and alternative payment methods should merchants consider when making hardware/software decisions?

Contactless payments will quickly become a competitive requirement for card issuers and card-accepting merchants as public awareness grows, and any stakeholders that delay consideration of these important questions will find themselves lagging behind this growing consumer trend.

Sources for US Data: Visa Investor Day 2020. “Contactless Payments Global Highlights,” Visa, Feb 2019. Federal Reserve Bank of Boston.

Sources for International Market Data: UK Finance. UK Cards Association. Payments Canada. Moneris. Reserve Bank of Australia. Visa and Mastercard.

This makes descriptive reference to trademarks that may be owned by others. The use of such trademarks herein is not an assertion of ownership of such trademarks by Accenture and is not intended to represent or imply the existence of an association between Accenture and the lawful owners of such trademarks.