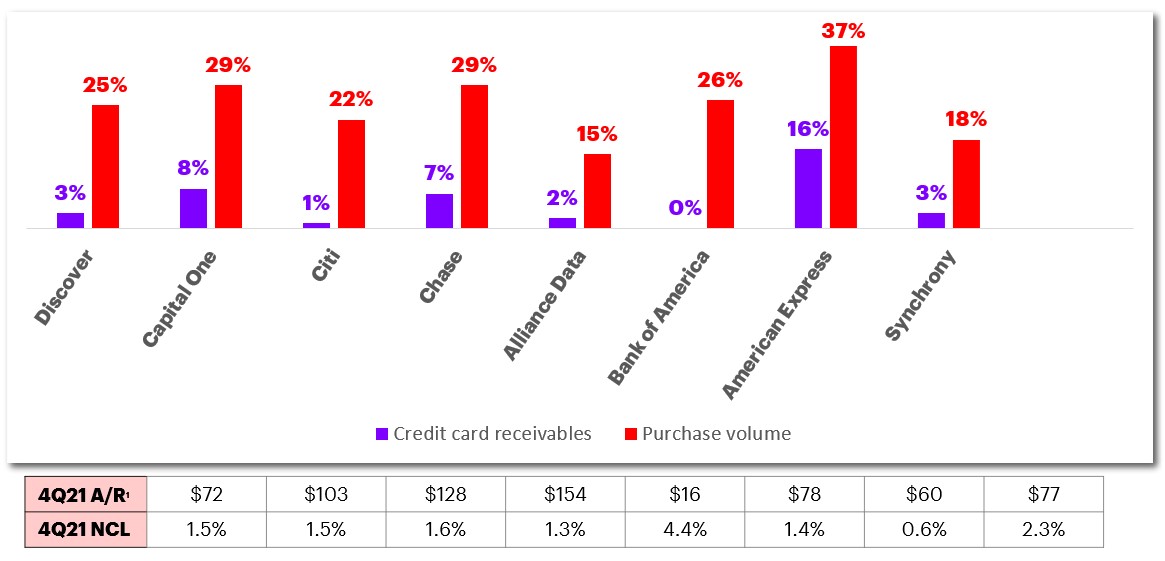

Credit card receivables & purchase volume YoY growth: 4Q21

1 Average Receivables in Billions. Note: Citi inclusive of both Branded and Retail Services. AXP is Revolving only. SYF A/R is Retail Card, NCL is total company.

Earnings call commentary

Growth

- “Consumer activity remains strong with credit sales up in the Q4 YoY. Our beauty and jewelry verticals remain the frontliners with holiday sales up more than 30% in each category. We saw particular improvement among millennials and Gen Z with spending and transaction activity during the holiday season exceeding pre-pandemic levels.” – Alliance Data Systems

- “Card acquisitions are driven by demand for our premium fee-based products where we saw acquisitions nearly double YoY. Millennials and Gen-Z are driving the growth in acquisitions.”– American Express

- “Consumers opened 3.6 million credit cards and grew card accounts in 2021 by more than any of the past four years. This helped card balances grow in Q4 despite payments remaining high.”– Bank of America

- “Domestic card revenue margin increased.. mainly due to from spend velocity, which is purchase volume and net interchange growth outpacing loan growth; and favorable YoY credit performance enabled us to recognize a higher proportion of finance charges and fees in fourth quarter revenue.” – Capital One

- “Combined, credit and debit spend was up 27% versus the fourth quarter of ’19, with each quarter in 2021 showing sequential growth compared to 2019. Card outstandings were up YoY but remained down 8% versus 4Q ’19. However, it’s promising to see that while revolving balances bottomed in May of 2021, since then, they’ve kept pace with 2019 growth rates.” – Chase

- “We’re encouraged by underlying drivers in both cards businesses, but payment rates do remain stubbornly high.” – Citi

- “The growth in receivables was largely driven by card… The primary drivers of YoY growth were continued strong sales volume and significant new account growth throughout 2021.” – Discover

- “In this past year, we achieved ~25 million new account originations and record purchase volume of $166 billion and a 19% increase in spend per active account.” – Synchrony

Credit quality

- “Payment rates trended higher for the quarter. Card balances still remain well below the pre-pandemic levels of $95 billion, and we continue to push that opportunity.” – Bank of America

- “One thing I would say about payment rates, though, is how broadly across the spectrum of our card business that we have seen payment rates increase over this period of time.” – Capital One

- “There’s no really large change in our credit risk appetite… The trajectory of normalization of card net charge-offs through the course of 2022 assumes that we get back to low threes around the end of 2022 or early ’23 in terms of card net charge-off which is in line with our expectations.” – Chase

- “Strong credit performance continued across all products. Card net charge-offs were down 113 basis points from the prior year and personal loans were 158 basis points lower.” – Discover

Partnership/product

- “We signed several new brand partners in the fourth quarter including the National Football League… Michaels… B&H Photo… and TBC.” – Alliance Data Systems

- “We’re monitoring the changing BNPL landscape, particularly in SplitPay. The consumer economic, competitive and regulatory landscape is continuously changing. However, most of our platform, businesses and pipeline opportunities are aligned with our digital installment lending product where the returns and growth opportunities remain strong.” – Alliance Data Systems

- “I do not believe BNPL is targeted at our customers. We have Pay It Plan It, an offering that allows our customers the opportunity to be as flexible with their payments as possible, and it gives you the ability to pick your installments and pay it over time. And we’ve had some increasing usage here, but it’s not a major driver of our growth.” – American Express

- “We’re always looking for new opportunities on the payment side of our business. And there, the versatility of our capabilities, you saw some of that with our partnership with Sezzle in terms of our ability to provide easier connectivity to merchants. On the payment side, both in the US and globally, we’re looking for opportunities.“ – Discover

- “During 2021, we added 36 partners and renewed another 38… We acquired Allegro Credit, a leading provider of POS consumer audiology products, deepening our foothold in the health and wellness space.” – Synchrony

Digital

- “Our payments platform provides new opportunities to deepen our relationships, expand our total addressable market and have provided new strategic relationships with RBC, Fiserv, Wayfair and Sezzle. These partners leverage our fintech platform to expand and improve the customer experience, while also offering greater payment choices to consumers.” – Alliance Data Systems

- “Half our consumer sales were digital in the fourth quarter. 86% of all the check deposit transactions are now digital. Customers use Zelle to transfer $65 billion in the most recent quarter.” – Bank of America

- “We are essentially fintech at scale. We have an unbelievable amount of data that we have collected; that allows us to manage big data and machine learning in real time to create opportunities at the forefront of how banking is being transformed.” – Capital One

- “On the retail side, we’ve been able to digitalize existing product offerings with applications like Chase MyHome and launch a cloud-native digital bank with our recent Chase UK” – Chase

- “We’ve been focused on how we drive installment lending activity, and we’ve seen significant growth in our Flex Loan and Flex Pay products as we’ve targeted customers who have historically been transactors. 90% of total installment sales are in digital sales, which is a low-cost acquisition approach.” – Citi

- “We upgraded our SyPi platform, including several new features like digital wallet provisioning and enhancements to push notifications and e-bill.” – Synchrony

Outlook

- “We also plan for higher marketing expenses in 2022 as a result of portfolio growth, new partnerships and new products. Information processing costs will increase as a result of our ongoing technology modernization, including the conversion of our core process to Fiserv this year.” – Alliance Data Systems

- “Our outlook remains constructive, but our reserve balances still account for various sources of uncertainty and potential downside as a result of the remaining abnormal features of the economic environment.”– Chase

- “For the upcoming year, we expect robust consumer demand, supporting broad-based purchase volume growth across industries and markets we serve. As consumer savings begin to decline and payment rates moderate, we’d expect purchase volume growth to moderate somewhat.” – Synchrony

Reserves/provision

- “Provision was a $489 million net benefit in Q4, driven primarily by asset quality, and macroeconomic improvement, and was partially offset by loans growth.” – Bank of America

- “We released $50 million from reserves during the quarter, driven by the continued strong credit performance of our portfolio and the relative stability of the macroeconomic outlook.”– Discover

- “When we think about the composition of the allowance, the first thing is just our expectation of our future losses and recoveries and our outlook assumes relatively swift normalization of losses from today’s unusually strong levels. The second factor is just qualitative factors. Today, those qualitative factors remain elevated to account for the remaining uncertainties around the pandemic and the economy.” – Capital One

Source: Bank quarterly earnings reports and earnings call transcripts.

Copyright © 2022 Accenture. All rights reserved.