Other parts of this series:

My first two posts in this series discussed digital banking’s moving goalposts and how the fragmentation and componentization of financial services are disrupting the traditional, vertically integrated business model for banks. Should banks throw away that model and replace it with one that looks more like a fintech? Not necessarily.

As we explain in our report on the Future of Banking, those existing models still hold value and can continue to provide the lion’s share of a bank’s profitability. But banks can no longer stop there. In the coming years, they will benefit from expanding their thinking and simultaneously implementing a kaleidoscope of business models. Banks that take this approach will have the opportunity to differentiate their products in the sea of sameness, and to do so in a cost-effective way.

The non-linear bank

The leaders of the future will be able to formulate and operate adaptive, profitable business models—such as indirect digital distribution and product bundling—while running their traditional vertically integrated business at the same time. Simply put, banking leaders will need to be better multi-taskers and juggle several business models while keeping their eyes on every ball.

To establish what those business models might look like, banks will have to:

- Delayer their internal capabilities and componentize individual products;

- Analyze each product to establish its value and pricing; and

- Turn those capabilities and components into new sellable units that are self-sufficient and cost-effective.

Those units can be offered to customers through partnerships with other types of providers. The micro-components can also be reassembled into new product offerings from the bank and sold directly to customers.

The future of banking: Time to rethink business models. An Accenture report outlines new banking business models that enable banks to reconfigure themselves to keep pace with disruption.

LEARN MOREThis non-linear approach to selling products and capabilities can help create new revenue streams for banks, without sacrificing their core business. Due to potential cannibalization risk we also observe these models are preferred for new market or for new customer segment entry. It releases the untapped value of the bank’s products and identifies their hidden costs as well. This more adaptive way of doing business also increases banks’ ability to compete head-to-head with digital natives in the industry. If banks do not define the principles which model they want to play in responding to the potential demand for collaboration from non-banks who need banking services they can be commoditized easily. While if they are ready to play non-linear options and define the adaptive strategy they can lead these models to untap value.

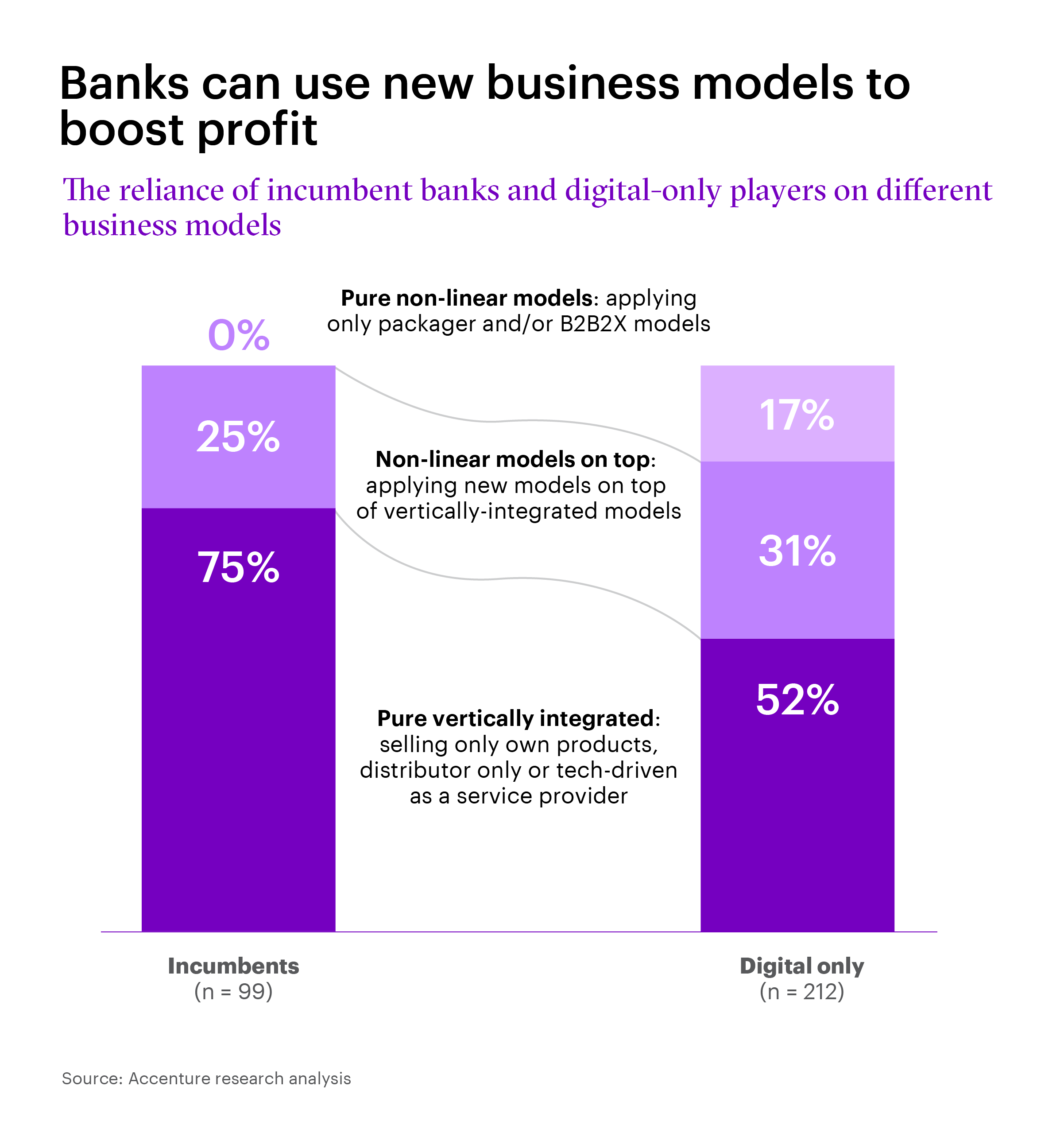

48% of leading digital-only players have adopted non-linear models, while 52% still emulate the traditional vertically integrated models.

Non-linear business models are already popular among digital-only players, with nearly half of them either applying them on top of vertical integration or using only non-linear models. Incumbents have been slower to adopt this approach, with 75% of them still using only the vertical integration model. While few incumbents are likely to phase out their traditional model entirely (and according to our research none have done this yet), the number of them adding non-linear models to their strategy is expected to grow sharply in the coming years.

Focus on value creation

To grow and be profitable, it’s no longer necessary for banks to always own the value chain end-to-end or to create all of their own products. What matters more is how they can create value—either for their own customers or for other players in the value chain. By thinking of every link in the value chain as a potential customer, banks can play a range of roles. Placing themselves in these multiple roles gives them the flexibility to create value in additional ways and capture growth from new sources.

Banks can do this by examining their current products and strategies and deciding which areas are:

- Core strengths: In these core areas, banks will continue to offer their own products. They can componentize their current products internally to reassemble and bundle them for direct sale to customers (business model: B2C).

- Bank services better delivered through a partner: Banks will identify certain products and services that would be better delivered through a partnership with another customer-facing provider, making the bank potentially invisible to the end user. These partners could be fintechs, super-apps or other digital players that prefer to outsource those products or services (business model: B2B2X).

- Third-party products delivered through the bank: Banks may decide that, in certain areas, they could provide better service to their customers, or decrease their costs, by distributing products from a third-party provider or bundling their own products with those of another provider (business model: packaging).

Depending on its size, market and strengths, a banking incumbent might embrace any one or a mix of these approaches.

Become a value architect

Banks that want to prepare for the future by shifting toward multiple, non-linear business models and roles in the value chain will require an open-minded vision and a methodical approach where they:

- See the bank’s products and services as individual components, decoupled from the traditional value chain;

- Reimagine the ways these components can be distributed and re-bundled for customers; and

- Continuously scan the financial services ecosystem to find the opportunities and partnerships that will provide the bank with maximum value for its products.

Banks that can architect value for themselves and their stakeholders in this way will have a chance to outperform the market.

To start exploring new business models for your bank, contact me. To learn more about the Future of Banking, read the full report, “It’s time for a change of perspective”.

Read report