Other parts of this series:

- The brave new world of Open Banking in APAC: Singapore

- The brave new world of Open Banking in APAC: Malaysia

- The brave new world of Open Banking in APAC: Hong Kong

- The brave new world of Open Banking in APAC: Japan

- The brave new world of Open Banking in APAC: Thailand

- The brave new world of Open Banking in APAC: Indonesia

Following the rollout of Open Banking regulations in the UK and the launch this year of the EU’s Payment Services Directive 2 (PSD2), countries across the Asia-Pacific region are following suit to establish their own frameworks to enable banks to share select customer data with third-party providers (TPPs), and TPPs to run transactions on customer accounts.

Regulatory developments

In 2015 Japan’s Financial Services Agency (FSA) launched a consultation desk to answer inquiries from fintech companies, which ran for 2.5 years, paving the way for broader regulatory reforms that set the grounds for the development of Open Banking in the country. The rationale for regulatory intervention has been to make payments convenient and accessible, to lower transaction costs and to address the issues outlined by the Bank of Japan (BOJ) Working Group on Financial Markets.

In the span of two years, the Bank of Japan (the central bank) amended the Banking Act twice. In April-May 2017 the BOJ changed the amount of ownership banks could have in fintechs to spur investment. A framework for regulating electronic payment service providers (covering both payment initiation service providers, or PISPs, and account information service providers, or AISPs) was also released, along with a registry of TPPs. Banks were required to publish their affiliation and cooperation with PISPs & AISPs by March 2018, while the amended banking act calls for 80 Japanese banks to open their APIs by 2020.

Meanwhile, the FSA in September 2017 established a FinTech Proof of Concept (PoC) Hub, which selects innovative projects and establishes a working group to bring products to the financial services industry. And in July 2018 the FSA launched a new regulatory arm, the Strategic Development & Management Bureau, dedicated to formulating a financial services strategy in which fintech is identified as a key initiative.

In general, regulation used in Japan to cover open APIs uses similar verbiage and definitions outlined by the EU in PSD2. The FSA has taken the approach to support banking transformation with the creation of implementation teams.

Key initiatives, opportunities & risks

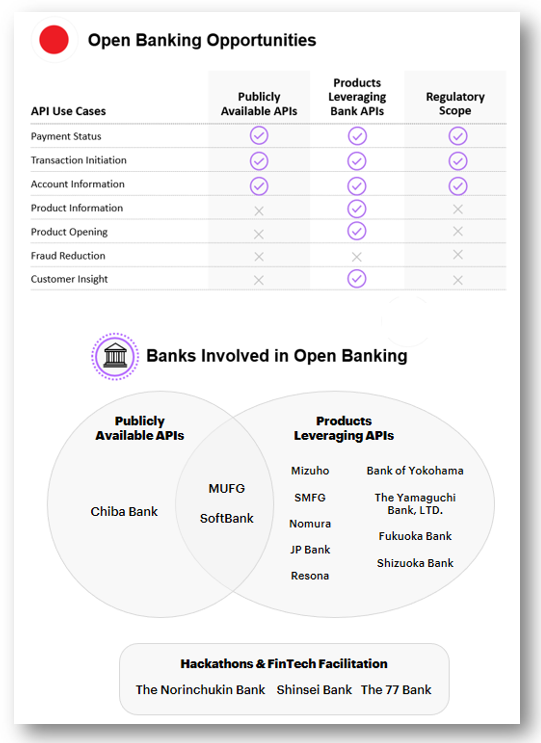

Due to the sheer size of the opportunity in Japan’s cash-based economy, banks’ API strategies have focused on digital payments and cashless transactions—demand for which is growing as the country prepares for the 2020 Tokyo Olympics. A variety of national and regional partners are teaming up to work with large payment-related fintechs to establish open payment schemes. Another salient feature has been that banks have established partnerships without building the kind of API portals observed in other markets.

Key market initiatives include, as early as February 2016, tech company Softbank and IBM teaming up and opening six APIs, geared towards Machine Learning using natural language processing. The following year, Mizuho Bank announced a partnership with SORACOM to develop a fintech payments platform specifically for IoT devices (for which trials were scheduled to begin in May 2018). And in April 2017 Japan’s largest bank, MUFG, launched a developer platform with APIs for retail and corporate banking, investments and trading.

A significant development came in October 2017 with the agreement of the three megabanks—MUFG, Sumitomo Mitsui and Mizuho—on a unified QR payment system aimed to launch in fiscal 2019. More recently, in May 2018, Fukuoka, Yokohama and Resona Banks (each among the top 10), collaborated to develop a QR code payment and settlement system called Yoka Pay. And in July, Softbank announced it was partnering with India’s leading fintech payments provider, Paytm, and Yahoo, to launch a QR code-based payment system in Japan.

Other initiatives include Nomura Holdings’ 10-week fintech contest, after which in November 2017 the company selected eight startups to co-create applications that leverage banking APIs. In addition, in May 2018 MUFG announced a partnership with Akamai, a US tech security company, to develop their own cryptocurrency, pegged to the yen, for instant payments.

While many related initiatives have been exploratory and are at the development stage, some noteworthy initiatives have been launched. These include Sumitomo’s partnership with bitFlyer, Japan’s largest bitcoin exchange, to allow their banking customers to transfer money in and out of the cryptocurrency market easily.

Given the ubiquity of cash in Japan’s economy, the focus on payments is understandable but does present some risks. Banks are extremely focused on payments compliance with little focus on the broader potential of Open Banking. The potential of Open Banking ecosystems as a business model might hence be neglected—and left open for tech giants to capitalise on.

Still, with so few developer portals, Japanese banks have an opportunity to leverage innovative ideas outside of payments—and learn from rich experience from other experienced markets (EU, UK, other AAPAC countries). Many banks have decided to work together when becoming payment-compliant, opening the door for large Open Banking ecosystems in the future, and the opportunity to collaborate with fintechs.

This article was written in collaboration with Ewa Wojcik, Sam Waldman and Hakan Eroglu. Many thanks for their input, research and analysis.

Accenture at Sibos

We’ll be discussing Open Banking and other topics at Sibos. Come see us at our booth and join us in the conversation around enabling the digital economy. Keep up to date on all the latest from us around Sibos right here on the blog.