Other parts of this series:

In this blog – the second in this two-part series – I’ll look at how banks should respond to the shifts happening within trade and supply chain finance due to market forces and COVID-19.

In my previous blog, we discussed the upending of supply chains, and saw how the geopolitical landscape and economic fallout from COVID-19 are further changing the supply chain context.

My conclusion was that banks must evolve their strategies to meet the needs of their fast-changing customer base – and they must do so as economies start emerging from COVID-19 lockdown, inducing customers to seek more working capital financing and traditional trade finance solutions.

Some banks are fortunate in that their core capabilities mean they’re well-placed to navigate the requirements of this fast-changing market. These advantages include liquidity, branch networks and trusted brands, all of which can also help them to hold off digital challengers. However, they need to maximise those strengths – and, of course, many don’t have them in the first place.

Ditch paper, embrace tech

As outlined in our recent publication on global trade, one crucial area is for banks to be geographically agile as this will ensure they can offer relevant solutions to clients who might move production to new markets. This requires that banks adapt their regulatory, network and branch reach, which are often key competitive differentiators. However, many have yet to do this.

Another area is trade finance, which remains overwhelmingly paper-based. Maximizing the potential of digitisation and modernising back-office processes will benefit banks and their clients by creating efficiencies, enhancing safety via automation (which is essential in the context of COVID-19), increasing security and helping to build customer trust.

Solutions here include robotics, artificial intelligence, data analytics and open APIs. Harnessing the potential of these technologies is key, not least because digitally agile challengers and neo-banks are eyeing the market. In addition, applying these technologies can help banks better manage their own risk and exposure.

Looking inward is important too – for example, banks should look to securitise supply chain loans to create monetizable assets. And they should be aware of external developments, like the surge in demand for Environmental, Social and Governance (ESG) initiatives, and the fact that the popularity of ESG solutions reflects growing customer concern around supply chain failings.

Tricky climate

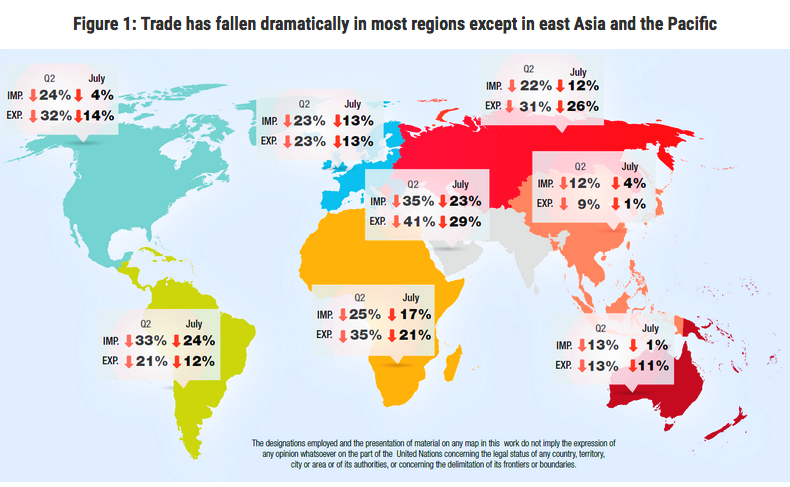

In short, many banks have much to do, and they need to take action in a difficult economic climate. Globally, year-on-year trade volumes fell steeply in most regions (see Figure 1), though they have shown tentative improvements in the third quarter as nations started to emerge from lockdown.

The global year-on-year decline in trade (Source: UNCTAD, October 21, 2020. Calculations are based on national statistics; data excludes intra-EU trade.)

The most encouraging signs come from China, where exports rebounded strongly in the third quarter. Another positive development was the November 2020 signing of the Regional Comprehensive Economic Partnership (RCEP) by 15 nations (including China), which creates a huge regional trade zone with vast potential.

Additionally, the development of several vaccines to tackle COVID-19 has boosted markets, though it remains to be seen how quickly those benefits will feed through. And the new US administration might bring in a more conciliatory tone to US-China trade tensions (although it’s unclear how this would affect tariffs between the world’s two largest economies).

In other words, despite tentative signs of recovery, there is still a lot of uncertainty, and my view is that a return to pre-crisis trade levels is unlikely before at least 2022.

Compounding the situation is the global reduction in monetary easing. As a result, under-pressure customers will require more credit and flexibility from banks, which in turn must adapt to a supply chain financing context that has changed hugely – and perhaps forever. In short, these are still tricky times. However, those banks that act fast will position themselves strongly for the future.