The top 15 global banking giants are generating their combined revenues and profits at a pace that’s well ahead of the average performance of their smaller competitors. What’s more, these big “winning banks” are harnessing their vast investments in digital technologies to help accelerate their growth. The success of these global giants provides valuable lessons for other financial institutions – particularly banks that are addressing growth markets.

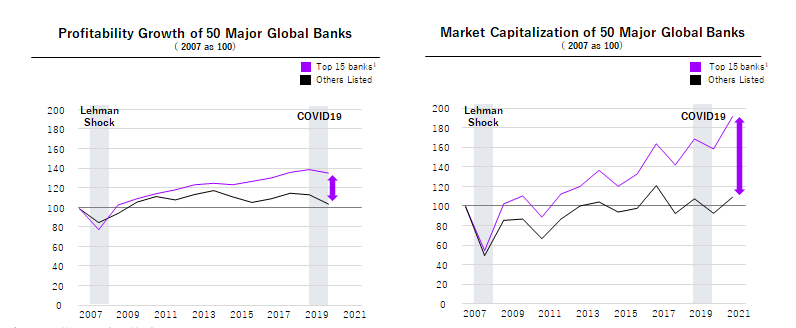

As our data demonstrates, a big divide is emerging between the global banking giants and the other 35 institutions that make up the world’s top 50 banks. The group of 15 industry leaders is increasing its profitability and market capitalization ahead of the combined performance of the other major global banks.

Multinational banks that are trailing the giant winning banks, particularly those serving growth markets, need to move quickly to avoid being further eclipsed by the global powerhouses. They cannot match their technology spend, but they can emulate some of their successes. Far-sighted institutions can transform themselves into winning banks. They can boost their revenues and profitability by adopting some of the business models and technology strategies implemented by the top 15 global giants.

Winning bank strategies

Let’s look at where the big winning banks are using innovative business models and advanced digital technologies to help boost revenue growth.

- Asset and wealth management: After transforming much of their retail business using cloud services such as banking as a service (BaaS), Morgan Stanley, MUFG and other progressive banks are using these technologies to overhaul their asset and wealth management activities. Revenues from asset and wealth management are set to soar in the next few years.

- Digital banking: Several major banks have launched successful digital banking businesses to compete with an array of fast-growing neobanks. BBVA and Standard Chartered, for example, are using their digital channels to deliver a range of simple low-cost banking products. The rapid acceptance of these products, especially among young consumers, will soon provide big banks with new revenue streams.

- Transaction banking: Large banks are using their technology infrastructures to deliver third-party services to corporate customers. Goldman Sachs, for instance, is using application programming interfaces (APIs) on its transaction banking platform to offer its corporate customers access to a wide selection of banking functions.

- Trade and supply chain finance: Several winning banks, including HSBC and Standard Chartered, are working with cloud computing service providers and fintech firms to offer small businesses cloud-based finance transaction processing. Their offerings will initially address trade and supply chain finance. But they are likely to be extended to include other banking services.

- Technology service provision: Digital technology has become so critical to the success of winning banks that some of these big institutions are reconfiguring themselves as technology companies. JPMorgan Chase, for example, plans to spend US$12 billion on technology this year and considers itself a “technology disruptor”. By recasting themselves as technology companies, rather than traditional banking institutions, winning banks can market their technology-intensive financial services more effectively. They can also strengthen their recruitment and retention of scarce technology skills. Growth market banks DBS Bank in Singapore and Siam Commercial Bank in Thailand have already transformed themselves into technology companies. Others will follow soon.

- Technology innovation: Big winning banks, such as JPMorgan Chase, HSBC and Goldman Sachs, have started investing in emerging technologies such as quantum computing, responsible artificial intelligence (RAI) and Web3/DeFi applications. These early investments will give the big institutions a head start in integrating such innovative technologies in their banking applications and products.

While the financial services market continues to be challenging, the big 15 global banks have shown how digital technology can be applied to create new business opportunities and help enhance revenue and profit growth. Smaller banks do not have to be left behind. By concentrating their technology resources on sectors where they can gain a competitive advantage, they can secure new markets and help bolster revenues and enhance profitability.

In my next blog post, my colleague Soichiro Muto and I will discuss the importance of digital banks in global growth markets. If you would like to know more about how to become a winning bank, please contact me here.

Get the latest blogs delivered straight to your inbox.

Subscribe