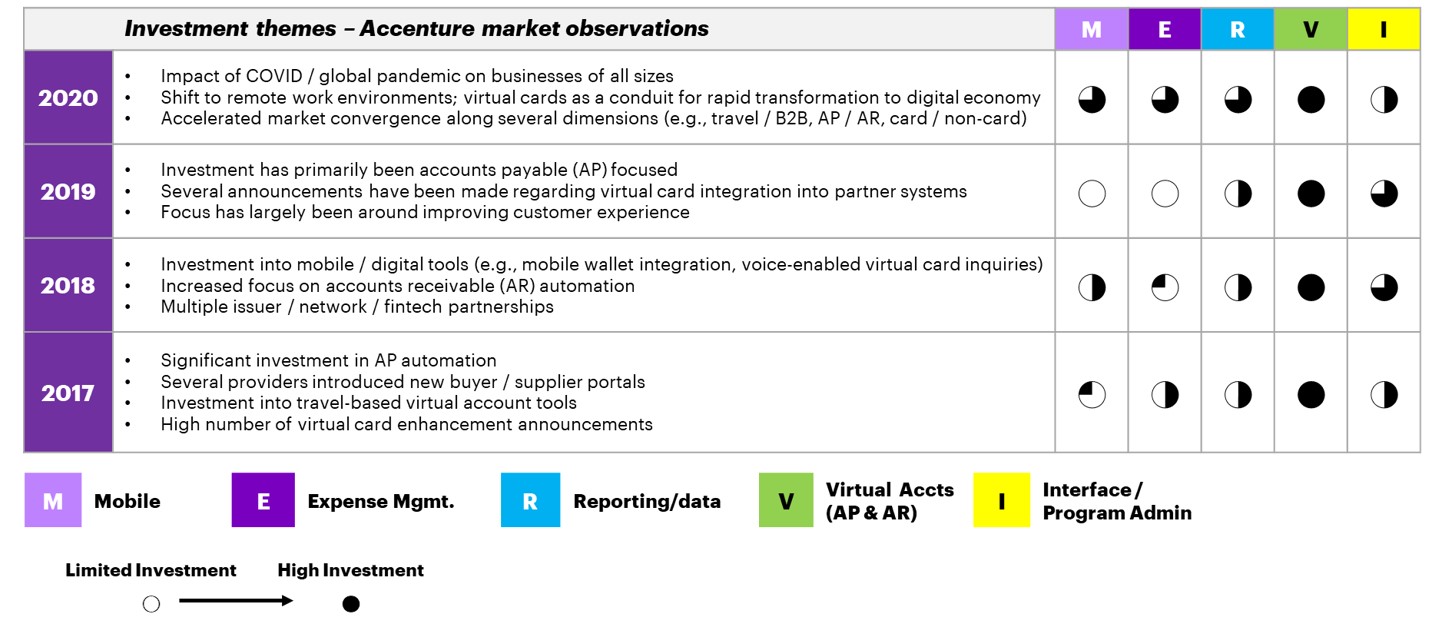

COVID-19 has had a profound impact on businesses of all sizes. Over the past 12 months, organizations across the globe have faced substantive impacts to their receipts, disbursements, and in consequence, liquidity. As organizations pivot to the new normal – remote workforce environments included – technology is helping to power their transformation. In our recent global research study of CFOs, more than three-quarters (76%) of respondents said that the COVID-19 crisis highlighted the valuable role that finance teams globally played in feeding early operational and financial warning insights and 79% said that the effects of COVID-19 have compelled them to ramp up their technology transformation. Business-to-business (B2B) payments providers have taken notice and are investing in new product offerings designed to meet the evolving digital needs of business clients.

Virtual cards have been a high-growth product for several years, and the pandemic has only accelerated that trend with 25% growth projected through 2025 in our baselined forecast. In the past year, financial institution, network, processor and fintech providers have invested in new virtual card solutions for a wide variety of use cases. Historically, these products have primarily been used for invoice-based payments made to suppliers; investments being made are expanding their utility and value.

Increased usability & access

As an example, an increasing number of virtual card offerings allow companies to provision single-use 16-digit account numbers directly into employees’ mobile-wallet solutions. The ability to provide contactless payment options in real-time is increasingly important in a post-COVID world, with many organizations expecting to continue operating on a remote basis for the near future. This instant provisioning provides access to more types of purchases and more potential users directly at the point of interaction (via mobile, online, or contactless in-store payments). For example, an employee with an urgent need (e.g., car service to repair blown tire) could digitally request a virtual card from his program administrator and have that card delivered to his mobile device within seconds, to pay specifically for the service. These cards can also be expanded to non-employees (e.g., contractors) for non-invoice-based purchases (e.g., buying lunch on a contracted work trip). With new end-users using these cards for new purchase types, growth is expected to accelerate.

Improved customer experience

The ability to push a virtual card to a mobile wallet provides an experience similar to what a business user would expect as a consumer, which is becoming increasingly important as digital natives increase as a share of the workforce. The accompanying real-time data associated with these purchases also simplifies the expense reconciliation process, reducing headaches for employees. Beyond mobile wallet usage, B2B payments providers are seeking to further integrate virtual payment (card and non-card) offerings into end-user organization financial systems. With the prevalence of intuitive consumer products that consolidate payment activity (e.g., the Apple card), more and more businesses desire real-time visibility into all of their payments in a single solution. Providers who give organizations the ability to make a payment to any supplier and review all payables and receivables activity in real-time, in a unified manner, will be positioned to create positive customer experiences across different businesses and business-stakeholder personas.

As broader payments initiatives (e.g., banking-as-as-service, instant payments, new ISO2022 standards) continue to roll out, B2B payments will become increasingly integrated and invisible. Businesses are expecting digital payment tools that combine real-time data, enterprise standards and consumer-like experiences. Providers who are able to adapt to the new world and build these kinds of solutions will be well-positioned going forward in the new digital normal.