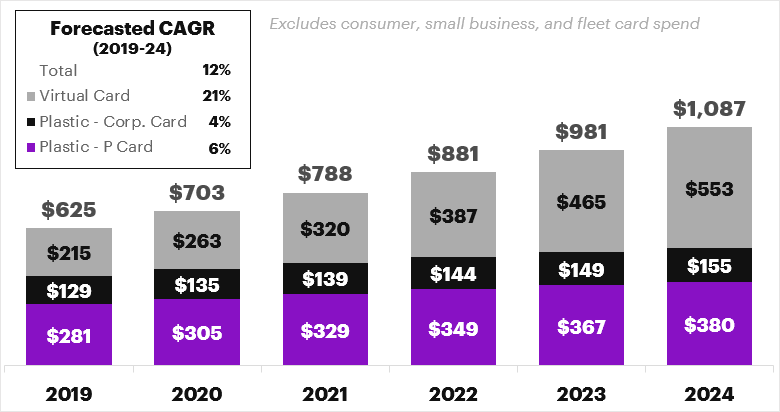

US commercial card spend grew an estimated 13 percent in 2019 and strong growth is expected to continue through 2024. Long-standing and emerging commercial card providers are developing innovative strategies to move more spend to card-based products, and broader B2B payment trends are anticipated to both blur the lines and buoy growth.

U.S. Commercial Card Spend¹ ($ billion)

Providers are developing and delivering more integrated and comprehensive card-based tools through multiple channels, driving growth.

- In Q4 2019, multiple products with strong digital/virtual foci were launched by issuers and fintech providers, with new features linking cards to depository-related accounts, bundled pricing with card acceptance, accounting & expense management integration, vertical-specific tailoring and working capital flexibility.

- Sophisticated providers are utilizing innovative platform channel constructs and value chain partnerships to reach new clients, route more efficiently and generate incremental commercial card spend.

- Many issuers are pursuing integrated payables and receivables strategies across card and non-card products to both broaden and deepen client relationships.

Beyond card, B2B payments are becoming more consumer-like, and the increased importance of intuitive digital tools bodes well for card-based products.

- The desire for simplified, automated and optimized experiences among commercial clients is combining with market innovations to accelerate shifts in providers’ operating models and go-to-market strategies.

- User-centric design, next-gen e-/m-interaction points and infrastructure modernization (e.g., real-time payments, ISO 20022, B2B e-commerce) are converging with process, platform and workforce transformation.

- As payments become increasingly digital, providers are evaluating future-state business models, with a range of partnership models becoming increasingly common to support use cases and reduce friction across the corporate journey (e.g., CFOTech, trade finance, liquidity and spend management, cross-border payments).

Boundaries are blurring between card and non-card products as payment products become more integrated in e-commerce and AP/AR platforms and end-user organizations continue to push for more intuitive B2B payment processes. B2B acquiring solutions, enhanced ACH/alternative B2B networks, and new form factors are gaining traction in the market. As a result, card and card-like virtual payments, more broadly defined, are on an accelerated path to $1T, with further room to penetrate the roughly $30T domestic commercial spend market.

The next wave of innovation is coming—it will be in B2B. Providers take note.

For more information or to discuss the opportunities within commercial card growth for your business, please contact us:

Frank Martien, Managing Director, frank.martien@accenture.com

Brian Rutland, Senior Manager, brian.rutland@accenture.com

Tom Skomba, Manager, tom.skomba@accenture.com

1Accenture estimates and analysis based on Accenture market data and knowledge as of time of this publication. Virtual Card spend includes vcard, epayables, EAP, and other IP-protected or commonly used terms for non-plastic card accounts often integrated with AP and/or ERP systems. To reflect the ongoing evolution and diversity of non-plastic digital payments, virtual cards defined herein also include virtual cards used with online travel agencies (OTAs) and proprietary closed-loop card systems.

Sources: Accenture proprietary commercial card sizing model, informed by data from Visa, Mastercard, and American Express annual reports, SEC filings, and investor presentations; UATP press releases; The Nilson Report, GSA SmartPay statistics, 2013 / 2016 RPMG Corporate Travel Card Benchmark Survey Results; the Federal Reserve Payments Study; U.S. Census data; Federal Reserve 2016 Payments Study.

I’d like discuss some of the things I see on your site… someone I could speak to?