Key themes

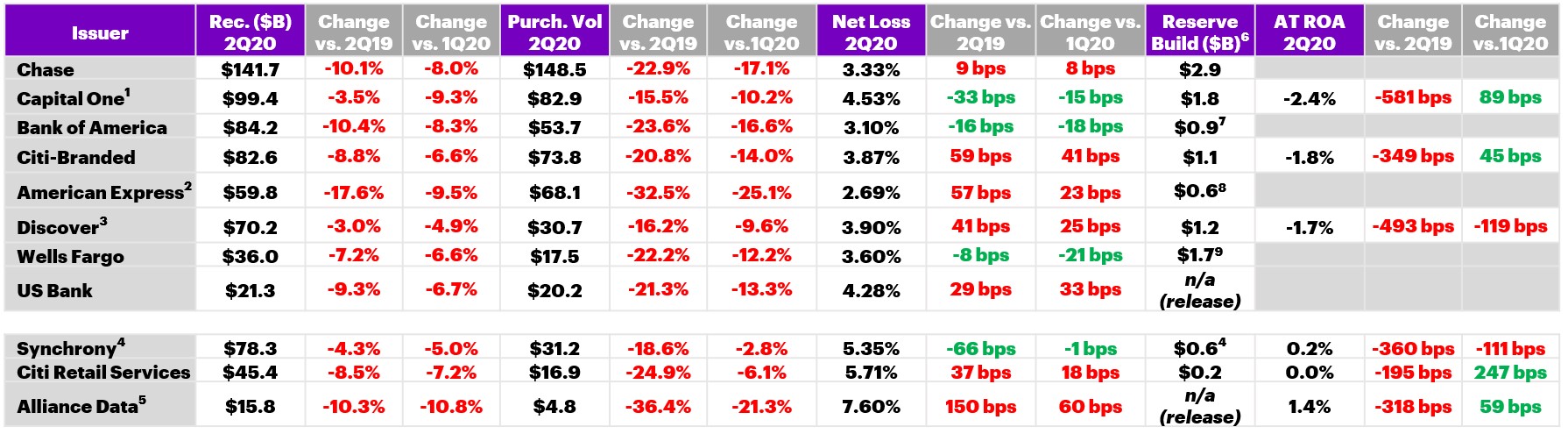

- The spending effects of the pandemic were fully felt in Q2 as most issuers report large declines in purchase volume between 15-30%, and receivables decline between 3-17% YoY.

- Alliance Data and American Express, in particular, experienced a 30%+ decline in spend YoY, driven by the headwinds of store-based retail (ADS) and T&E sectors (Amex).

- Credit quality remains stable, for now, largely as a result of forbearance/government stimulus programs; issuers generally expect losses to increase through 2020 and well into 2021, and most banks are forecasting unemployment rates to remain in double-digits into 2021.

- Similar to Q1, issuers increased reserves significantly to allow for potential future credit loss rate spikes; however, reserve builds were generally more modest than those observed in Q1.

- Issuer profitability continued to be pressured for the second straight quarter as a result of reserve builds and spend/receivables decline, though the average ROA was slightly better than Q1.

Notable happenings

New partnerships

Synchrony added a new PLCC card with Adorama; the Helzberg Diamonds program transitioned from Capital One to Alliance Data; Splitit partnered with Mastercard for global expansion; Klarna announced a partnership with Sephora.

Partnership developments

Synchrony announced that it renewed and extended several key relationships including CarX Tire & Auto.

New products/features

Synchrony and Verizon launched a co-branded Visa credit card; U.S. Bank launched its new Altitude Go Visa credit card with rewards categories tailored to the COVID-19 pandemic; Verrency announced the launch of a new installment lending solution; Apple announced that it will offer broader no-interest payment plans on the Apple Card; Walmart announced enhanced benefits for its reloadable debit card in partnership with Green Dot.

Mobile & tech

Walmart entered into a partnership with Shopify to expand its third-party marketplace site; U.S. Bank launched new B2B payments capabilities such as enhanced receivables visibility and streamlined invoice payments; Plaid launched a new API-management service for banks; PayPal launched a new QR Code functionality for in-store payments; BillGO launched a bill pay relief hub for consumers impacted by the pandemic.

Industry statistics (based on non-retail card issuers in scorecard section)

1Total receivables for all issuers below at end of 2Q20. 2 Total purchase volume of all issuers below in 2Q20, not annualized. 3After-Tax ROA of issuers that publicly report – Citigroup, Capital One, Synchrony, Discover and ADS. 4 YoY = Year-over-year change versus 2Q19.5 QoQ = Quarter-over-quarter change versus 1Q20.

Issuer scorecard ($billions)—Q2 2020

1Capital One is US consumer and small business credit cards and installment loans. Purchase volume excludes cash advances. 2 American Express changed its reporting method as of 2Q18; all figures are for US Consumer segment (revolving and charge products) which no longer reports net income.3Discover receivables, purchase volume (excludes cash advances), and losses are US domestic card only; ROA includes all of Direct Banking segment (credit card loans represents ~80% of Direct Banking loans). 4 All figures include all of SYF’s business lines (i.e., Retail Card, Payment Solutions, and CareCredit). Retail Card accounts for ~70% of total receivables. 5 Average receivables of $16.1B (does not include loans held for sale). 6 Credit card specific unless otherwise noted. 7 Consumer Bank. 8 Total company. 9 Community Bank.

This makes descriptive reference to trademarks that may be owned by others. The use of such trademarks herein is not an assertion of ownership of such trademarks by Accenture and is not intended to represent or imply the existence of an association between Accenture and the lawful owners of such trademarks.