Other parts of this series:

- Digitally Mature Banks: Why the Future’s in Their Hands

- COVID-19 Resilience, Digital Maturity and Outperformance

- Digital Maturity + COVID-19 Resilience = Strategy

- Digitise for Efficiency and Agility

- A future-ready approach: Building “Living Systems” for banks

- Restructure to Survive: How to turn around the weakest banks

- A future-ready approach: Journey to the cloud

- Banking’s cloud imperative: Succeeding in an altered landscape

This series of blogs looks at the future of banking in Growth Markets in a post-COVID-19 world. The first blog introduced our Digital Maturity Index, showed why highly digitally mature banks roundly outperform all others, and concluded that digitally mature banks are best-positioned for a post-pandemic world – with many Growth Market countries primed to go digital. In this blog, I’ll show why digital maturity alone isn’t enough.

It’s no surprise that banks ranked highest on our Digital Maturity Index (DMI) are best-placed for a post-pandemic world. Digitisation is banking’s future, as experts have advocated for years. Among them is Chris Skinner, who in July, for example, highlighted an article about the impact of COVID-19 and banking in the Financial Times titled: “When the banks closed in Wuhan, nobody cared”.[1]

Why didn’t the residents of Wuhan in China care?

“Because China has leap-frogged Europe and America from a payments and financial markets perspective … and has rapidly moved to become a cashless society,” Chris wrote.[2]

This digitisation drive, ranging from online banking to mobile wallets to payment apps like AliPay and WeChat Pay, is so embedded that people in China rarely need to visit their bank. That’s why, when banks closed it made little difference. As Chris noted, that wasn’t the case in Europe and North America.

This highlights a key point: COVID-19 shows there’s more to banking success than just being digitally mature. To that end, I’m going to take banking success a step beyond digital maturity by introducing another index we’ve developed: the COVID-19 Resiliency Index (CRI).

(I’ve no doubt that Chris, a prolific author and blogger, will weigh in on this; I’d love to hear your thoughts too.)

Introducing the CRI

We’ve written elsewhere that COVID-19’s impacts on industries globally have been serious, and we’ve outlined steps that firms can take to outmanoeuvre uncertainty.

Accenture’s advice includes actions banks can take as they seek to deal with its material and medium-term stresses: credit losses and revenue compression; costs misaligned with revenues; and having to adjust operational processes, including harnessing data analytics and extending ecosystem partnerships.

The pandemic has reinforced the imperative for banks to pursue a digital strategy. The CRI helps them by assessing five factors:

- Credit risk measured by the proportion of non-performing loans over the total loan portfolio;

- Revenue compression measures net interest margin; net interest income over total operating income; and trading income as a percentage of total operating income;

- Service and advice provision assesses the frequency of physical channel usage and the average customer importance of the digital proposition;

- Operating model and costs weighs FTE costs over average earning assets and non-FTE costs over average earning assets;

- Balance sheet assesses leverage (measured by average assets over average equity) and the liquidity coverage ratio.

These CRI calculations rank a bank’s resilience to the impact of COVID-19 as high, medium or low.

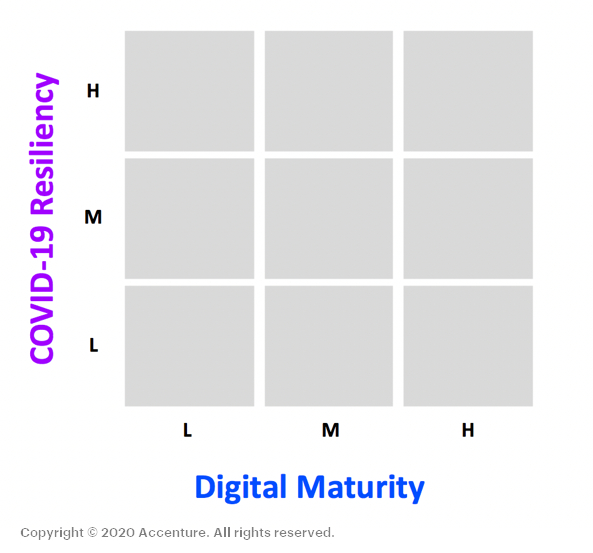

CRI, Meet DMI

Now here’s where it gets really interesting. Combining a bank’s DMI and CRI rankings lets us position it on our CRI/DMI matrix (see below).

Click/tap to view larger image

Where the bank lands on this matrix is crucial. Why? Because we believe that the combination of its digital maturity and its COVID-19 resilience defines the strategy it must take to emerge stronger and better-positioned. Employing the right strategy will also ensure it is robustly prepared for the next event.

Banks will find themselves primarily in one of three strategic segments:

Disrupt for Growth: some banks are in the enviable position of being highly digitally maturity and with medium-to-high COVID-19 resiliency. That positions them well for “Digital Act II”, in which they can disrupt through data, digital, ecosystems and new business models.

Digitise for Efficiency: these banks are further behind on the digital curve, yet are well-placed for COVID-19 resiliency. They are well-positioned to start on “Digital Act I”, initiating or accelerating their digitisation efforts across the end-to-end value chain to strategically improve their efficiency and agility.

Restructure to Survive: with the lowest resiliency to COVID-19, these banks face an existential threat. They must act fast by restructuring their balance sheet and cost base through focused expense reduction and asset sales, and should significantly reconfigure their operating model.

Knowing where their bank is positioned on the matrix gives the C-suite a head-start in plotting their strategic course ahead. The next blogs in this series will look more closely at this vital aspect.

Subscribe for more from Accenture Banking.

Disclaimer: This document is intended for general informational purposes only and does not take into account the reader’s specific circumstances, and may not reflect the most current developments. Accenture disclaims, to the fullest extent permitted by applicable law, any and all liability for the accuracy and completeness of the information in this presentation and for any acts or omissions made based on such information. Accenture does not provide legal, regulatory, audit, or tax advice. Readers are responsible for obtaining such advice from their own legal counsel or other licensed professionals.

[1] When the banks closed in Wuhan, nobody cared, Financial Times (May 5, 2020). See: https://www.ft.com/content/76291c8f-0ad0-472b-ac1e-bff1646bfb1a

[2] When the banks closed, no-one cared, The Finanser (July 30, 2020). See: https://thefinanser.com/2020/07/when-the-banks-closed-no-one-cared.html/