Other parts of this series:

- Digitally Mature Banks: Why the Future’s in Their Hands

- COVID-19 Resilience, Digital Maturity and Outperformance

- Digital Maturity + COVID-19 Resilience = Strategy

- Digitise for Efficiency and Agility

- A future-ready approach: Building “Living Systems” for banks

- Restructure to Survive: How to turn around the weakest banks

- A future-ready approach: Journey to the cloud

- Banking’s cloud imperative: Succeeding in an altered landscape

This series of blogs looks at the future of banking in Growth Markets in a post-COVID-19 world.

At Accenture, we believe each bank’s strategy for a post-pandemic world should be defined by its digital maturity and its COVID-19 resilience. Once the C-suite knows where their bank is positioned, they can apply the right strategy to emerge stronger and better-placed for a post-COVID-19 world.

As my previous blog showed, banks’ strategies will primarily (though perhaps not exclusively) fall into one of three segments:

- Disrupt for Growth

- Digitise for Efficiency and Agility

- Restructure to Survive

This blog will look at the strategies that banks in the first segment should employ. I’ll examine the second and third in future blogs.

From 2011 to 2019, the banking industry shifted from a position of vulnerability – its susceptibility to disruption – to one of volatility, a measure of its current level of disruption (which you can read more about in this blog). The COVID-19 pandemic has served to make matters more complex for an industry that was already underperforming.

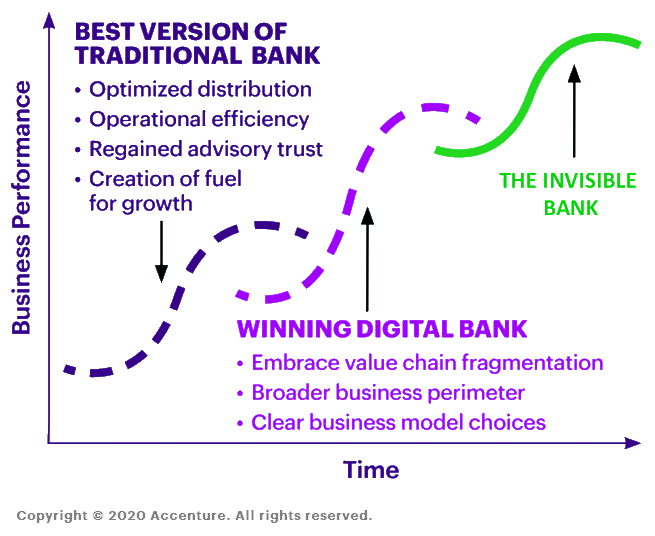

But, as our matrix makes clear, some banks have done much better in preparing for the digital economy than others. We’ve shown that leaders, whether banks or non-banks, are succeeding by implementing new business models that are moving them closer to delivering “invisible banking”.

They’re using data, open APIs and ecosystems to create new business models and unlock new value. In so doing, they’re

Invisible Banks, Visible Lessons

outperforming even “winning digital banks”, which embrace value-chain fragmentation, a broader business perimeter and clear business model choices. These leaders are better-placed then even the best version of a traditional bank. On their “Digital Act II journey” they’re employing disruptive strategies and building new business models that drive hyper-scale growth and target digital attacker economics.

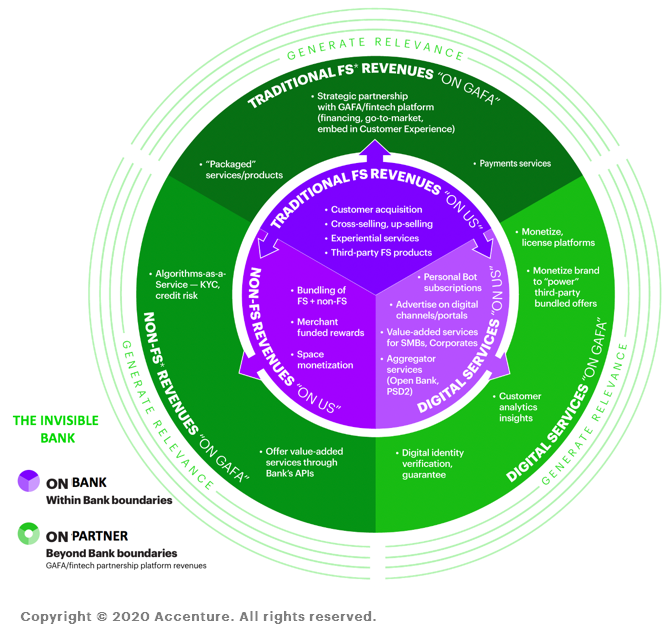

Invisible banking is a disruptive future business model that generates bank and non-bank revenues, and provides value-added digital services within the bank’s boundaries and in partnership with GAFA/BAT/fintech/techfin firms (see diagram).[1] Additionally, all of these services create relevance for their customers.

Take traditional bank revenues: invisible banks generate revenues internally from customer acquisition, cross-selling and up-selling, and selling third-party products. Externally they partner with GAFA/BAT/ fintech/techfin platforms, earning from packaged services and products, and payments services. This spread of revenue generation across boundaries holds for non-banking revenues and digital services too.

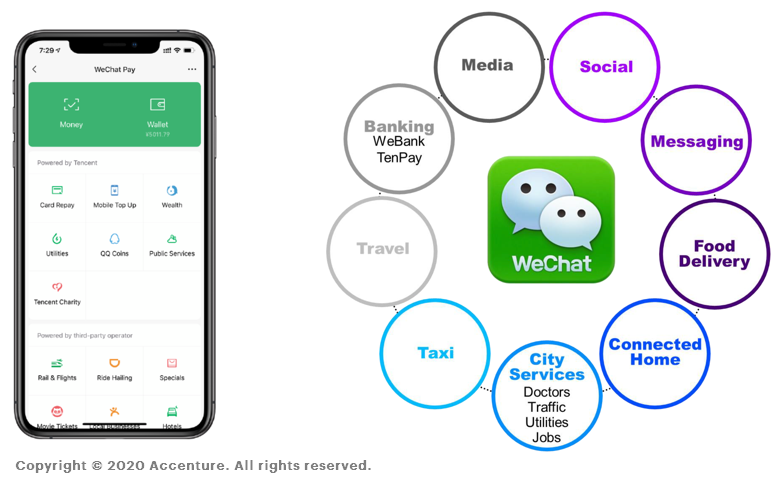

Arguably the preeminent model of invisible banking is WeChat. This super-app’s platform ecosystem encompasses nearly all of its users’ lives – from payments to social media, entertainment to services, travel to investing, and much more. Users operate seamlessly in every area of their lives without leaving the app, providing WeChat with massive data opportunities and revenue-sharing from partners. The approach of WeChat, which was founded in 2011, makes it an aspirational model for banks in a post-COVID-19 world.

With more than 1.2 billion users worldwide, WeChat is a colossus in the platform economy in China, and its position as a data-driven product champion is one to which every newly launched digital bank aspires.

For those looking to disrupt for growth, the implications are evident: first, clearly define what role you want to play in the “invisible bank” (e.g. balance sheet provider only, distributor, product manufacturer or all three); second, be specific in your partnering strategy, with a focus on the larger platform players; and third, prepare to open up by prioritising a modern data supply-chain and open-API development.

I believe that executives whose banks follow a Disrupt for Growth strategy will be well-positioned to emerge as industry leaders with a commanding – and perhaps unassailable – advantage over their peers. Those peers will face competition not only from these disruptive invisible banks, but also from the neo-banks that are emerging across the region.

Many of these peers fall into the second segment, Digitise for Efficiency and Agility. My next blog will look at the strategies these banks should employ.

Subscribe for more from Accenture Banking.

Disclaimer: This document is intended for general informational purposes only and does not take into account the reader’s specific circumstances, and may not reflect the most current developments. Accenture disclaims, to the fullest extent permitted by applicable law, any and all liability for the accuracy and completeness of the information in this presentation and for any acts or omissions made based on such information. Accenture does not provide legal, regulatory, audit, or tax advice. Readers are responsible for obtaining such advice from their own legal counsel or other licensed professionals.

[1] The GAFA firms are Google, Apple, Facebook and Amazon. The BAT firms are Baidu, Alibaba and Tencent.