Other parts of this series:

- Digitally Mature Banks: Why the Future’s in Their Hands

- COVID-19 Resilience, Digital Maturity and Outperformance

- Digital Maturity + COVID-19 Resilience = Strategy

- Digitise for Efficiency and Agility

- A future-ready approach: Building “Living Systems” for banks

- Restructure to Survive: How to turn around the weakest banks

- A future-ready approach: Journey to the cloud

- Banking’s cloud imperative: Succeeding in an altered landscape

This series of blogs looks at the future of banking in Growth Markets in a post-COVID-19 world.

It’s time to turn to the situation facing banks in the third of our three segments – Restructure to Survive. As the name suggests, they are in the least enviable position to emerge post-pandemic as viable businesses.

Adapt or Die-vest

![]()

The problem for banks in this segment isn’t their digital maturity – they might rank as high, medium or low on that score. The problem is that they’re far less resilient to the impacts of COVID-19 than their peers, and that’s left them with a host of challenges.

Three of the most common are an uncompetitive cost structure, low profitability and misaligned risks. Banks in this segment typically also have poor capital strength – and here I’m talking, too, about fintechs that are highly reliant on the infusion of new capital (or that are susceptible to regulators looking to rein in fintech activity).

COVID-19 has damaged even the strongest banks, of course, but its impact on banks in this segment has left them facing an existential threat. Survival requires that they:

- Restructure their balance sheets and cost base through focused expense reduction and asset sales

- Significantly reconfigure their operating models

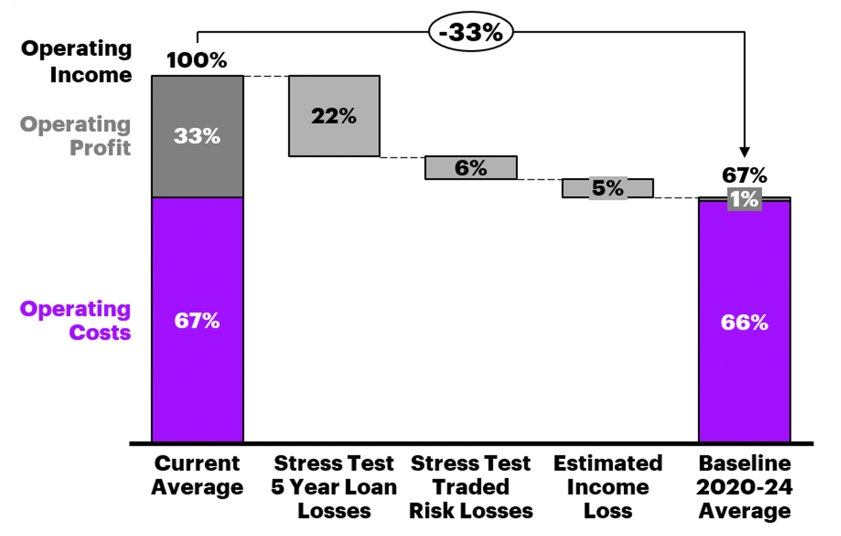

How serious is their situation? Consider this: an Accenture survey on the impact of COVID-19 on seven leading UK banks concluded that they need to cut costs by one-third simply to retain their current margins (see graph). Given that this proportion constitutes their entire operating margin, those that fail to act risk delivering zero aggregate profits before taxation for the period 2020-24.

If seven of the UK’s leading banks are in this position, it’s easy to conclude that banks in the Restructure to Survive segment are at far greater risk.

COVID-19’s impact means leading UK banks need a 33 percent cost saving to retain current margins. (Source: Accenture Research)

Action stations

Banks in the Restructure to Survive segment need to undertake at least one (and likely more than one) of the following actions.

1. Dramatically adjust their cost structure

Banks can transform their operating model by controlling variable costs. In many cases, that requires marrying outsourcing with intelligent operations.

We’ve written elsewhere about next-generation Human + Machine augmentation – using platforms and intelligent technology to drive automation and new growth. Coupling a tech-empowered workforce in this way with the right tools (like artificial intelligence) to leverage data can help banks cut operational and processing costs dramatically – by 20-40 percent in some cases. Banks might also be able to front-load some benefits by using third parties to monetise operations.

Banks wondering how and where to start can apply diagnostic tools to work out which operational areas are ripe for improvement. Those analyse a range of crucial areas, allowing the bank to determine the potential level of transformation and the best actions to take to realise value fast.

That can bring profound changes. We worked with a European bank that wanted to cut banking costs and operating risks while increasing productivity. Over a period of several years, its transformation programme

boosted efficiency and service quality. Productivity rose 45 percent, with 98 percent of processes monitored through a range of KPI and analytics solutions.

2. Divest underperforming businesses to improve profitability

Banks’ price book values are in many cases lower than 1, which is why many are offsetting the drag on ROE or constraints on capital by exiting underperforming businesses – whether operations in countries, specific business lines or both.

There are plenty of examples. A number of Australia’s biggest banks have divested their wealth and insurance businesses in recent years, and HSBC recently confirmed it was looking to sell its 150-strong retail branch network in the US due to its uncompetitive position, the impact of the pandemic and low-interest rates. The bank also said its French consumer banking arm was “in the final stages” of a potential sale.

A more extreme example was provided by Australia’s Xinja Bank, a neobank that began operations in late 2019 – and which handed back its banking licence little more than a year later, citing the impact of COVID-19 and “an increasingly difficult capital-raising environment”.

3. M&A

Merging or being acquired are options for banks that can’t raise new capital or restructure to maintain independent operations.

The banking sector has seen a wave of M&A activity recently. In Australia, for example, neobank 86 400 was acquired in early 2021 by National Australia Bank and will be combined with UBank, NAB’s digital bank.

That same month, Bank of Queensland acquired ME Bank, a neobank that had been set up by a consortium of industry super funds. Among other things, the deals show that incumbents have an appetite for such acquisitions, seeing it as a way to leapfrog digitally.

Surviving in interesting times

For undercapitalised banks and fintechs, the funding environment is likely to remain tricky in 2021. Interest rates will remain low, curbing revenues, even as the economic effects of the pandemic have made it harder to raise capital to shore up balance sheets.

That said, the impact will vary by geography, with players in economically resurgent regions like Southeast Asia better able to cope than peers elsewhere.

But that insulation is relative, and it doesn’t detract from the need to act.

As we’ve seen, intelligent operations offer a clear path to building a future-ready bank, with an improved cost structure and overall tech renewal. At the heart of that approach is the banking cloud journey – the subject of my next blog.